First of all a confession.

I have to admit, I genuinely enjoy watching Parliament debates — whether it’s PMQs or the Budget. I know I’m probably in a minority of one, and yes, the behaviour can resemble a room full of over excited school children, but for me it’s brilliant entertainment.

In yesterday’s Budget, I thought Rachel delivered a solid performance: confident, clear, with a few well-placed lighter moments. Kemi’s response, on the other hand, was noticeably sharper — perhaps even a bit brutal at times — but it was also a response that really landed. She certainly made her presence felt.

Winners

To be honest… I can’t see many. Nowadays, a “win” might simply mean not being hit.

1. State Pension Recipients

The 4.8% rise from 2026 is positive and will help offset some pressure from the cost of living.

2. ISA Users Who Diversify

Although the Cash ISA limit drops for the under 65s, the overall £20,000 ISA allowance gives savers room to make use of Stocks &Shares and other ISA types.

Losers

1. Higher Pension Salary Sacrifice Users

From April 2029, only the first £2,000 of salary sacrifice contributions avoids NI. Higher earners making larger regular contributions will face increased NI costs.

2. Anyone Earning While Thresholds Are Frozen

With income tax and NI thresholds frozen until 2031, “fiscal drag” will quietly pull more of your income into higher tax bands as wages rise—meaning a higher tax bill even without rate changes.

3. Business Owners Taking Dividends

Dividend tax increases by 2% from April 2026, so company directors and shareholders will see higher tax charges when drawing income this way.

4. Landlords and Property Investors

The new property income rates of 22%, 42% and 47% from 2027will noticeably increase tax bills for many landlords.

Thoughts

Whatever your view of the Budget, we knew that Labour would increase taxes rather than cut spending so this is no real surprise but the key takeaway for me is two-fold:

1. The constant speculation leading up to it benefits no one—retirees, employees, or business owners alike. I’m simply relieved it’s over. Yes, taxes are going up, but there were no drastic shocks or sweeping changes this time. It seems to me like death by a thousand tax rises. Let’s hope next year is a slightly calmer build up!

2. What I think is clear is that government of all colours can change the goalpost. I am not talking about drastic measure like no State Pension or privatising the NHS but I think it’s safe to assume the goal posts can change for example the State Pension Age increasing further of removing of the triple lock.

Some younger clients already approach things with this mindset. I’m often asked, “How much do I need to save each month to get to£1,000,000?” There’s no complicated science behind it — £1,000,000 simply feels like a solid, reassuring target. It’s the kind of number that gives you enough flexibility to handle whatever future government changes might come your way.

It goes without saying that you need the spare income in the first place to be able to invest. For many people this comes down to earnings or, in some cases, inheritance — but increasingly, what I’m seeing is the impact of lifestyle creep.

Lifestyle creep is what happens when your spending quietly rises in step with your income. You earn more… so without really noticing, you start spending more — nicer holidays, better car, more meals out, upgraded everything.

The problem?

Your savings rate doesn’t improve, even though your income does. Over time, this can massively shrink the amount of wealth you build.

Why Lifestyle Creep Happens

· “I deserve it” mindset after a pay rise or bonus

· Social comparison (“everyone else has upgraded…”)

· Subscription creep — small add-ons that accumulate

· Failure to adjust savings automatically when income jumps

Why It’s Dangerous

· Your spending can rise faster than your income

· Harder to cut back later once lifestyle expectations harden

· Retirement goals (like saving £1m) become much more difficult

· Makes it feel like you’re “never getting ahead” even with higher earnings

How to Protect Yourself

· Increase savings first whenever income rises

(e.g., “£300 pay rise = £200 into investing, £100 to lifestyle”)

· Automate investment increases so you don’t feel the friction

· Set ceilings on “upgrade” categories (cars, holidays, tech)

· Build identity around being financially intentional, not flashy

· Track spending trends— not obsessively, just enough to spot drift

The Healthy Version

Not all lifestyle improvement is bad. Enjoying your money matters. The goal isn’t to freeze your lifestyle forever — it’s to prevent automatic, unconscious upgrades that sabotage long-term goals.

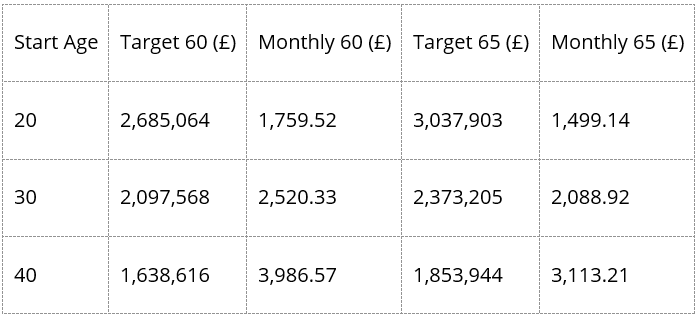

How much should an individual save to give them the best chance to reach a £1,000,000

The table shows the inflation adjusted £1,000,000 target and the monthly savings required, assuming a 5% investment return.

There’s no getting away from it — some of the monthly savings’ figures are large. The good news is that pensions make this much more manageable. Even basic-rate tax relief reduces the real cost by 20%, and for employees, employer contributions can bring that figure down even further.

For example, a 30-year-old needing to save £2,088 per month in theory would see their personal contribution fall to around £1,670 before basic rate tax relief is added — and that’s before taking into account what their employer might add on top.

Of course, for many people in their 20s, 30s and 40s, saving at this level simply isn’t realistic. But there are individuals with the income and flexibility to make a conscious choice: allow lifestyle creep to absorb those extra earnings or redirect some of that surplus to reduce future reliance on the government and build greater financial independence.

For anyone already retired or close to it, this won’t really apply — you’re essentially where you are. But please do feel free to pass this on to anyone younger who you think might find it useful and at least food for thought!